Share

In today's rapidly evolving technological landscape, the insurance industry finds itself at the forefront of a transformative wave, leveraging the power of big data to revolutionize traditional practices. Big data, characterized by its vast volume, velocity, and variety, has emerged as a game-changer, reshaping how insurers understand risk, personalize policies, and enhance customer experiences.

Understanding Risks and Predictive Analytics

At the core of insurance lies risk assessment, and big data serves as a goldmine for insurers in this realm. By analyzing immense volumes of historical and real-time data, insurers can gain deeper insights into risk factors such as demographics, geographic data, socio-economic indicators, and even data from IoT sensors.

These insights enable the development of more accurate predictive models. Machine learning algorithms crunch through these vast datasets to predict the probability of claims, fraud detection, as well as identify trends. The ability to foresee risks more accurately not only helps insurers better price policies but also mitigates potential losses, ultimately benefiting both the insurer and the insured.

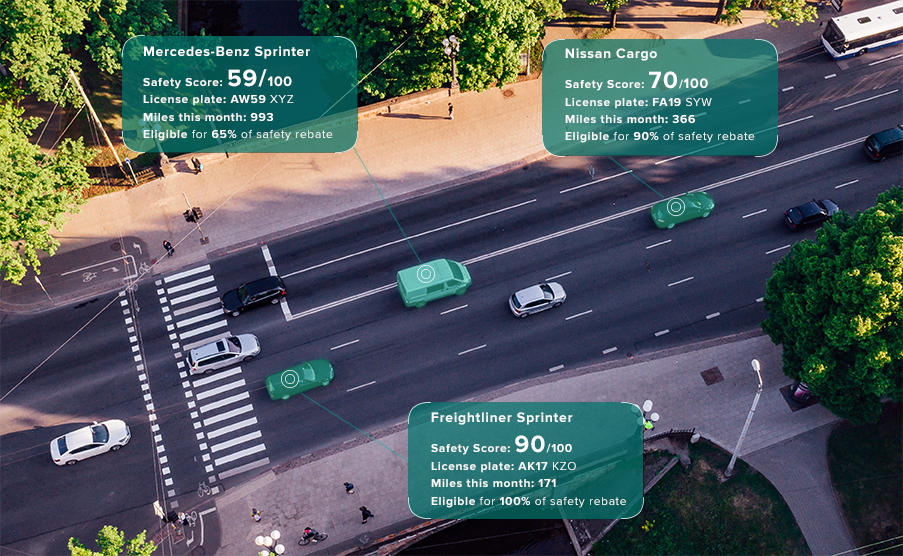

A great example is Flock. The company uses real-time data and a risk intelligence engine to accurately assess risk on a per-fleet basis. By analyzing the data, they provide fleet managers with insights to improve safety and reduce the cost of insurance in the long term.

Customizing Policies and Personalization

One-size-fits-all insurance policies are becoming a thing of the past. Big data empowers insurers to tailor policies to individual needs. By analyzing customer data and behavior, insurers can create personalized offerings that better match specific lifestyles, preferences, and risk profiles. For instance, usage-based insurance (UBI) models in auto insurance use telematics data to price policies based on driving behavior, rewarding safe drivers with lower premiums.

Usage-based insurance is popular in the motor insurance segment. Companies like Ticker and ByMiles implemented a usage-based insurance (UBI) program using telematics data collected from customers' vehicles. By analyzing driving behavior, they personalized premiums based on individual driving habits such as speed, braking patterns, and mileage.

Usage-Based Insurance - Illustration

Usage-Based Insurance - Illustration

A significant number of drivers are switching from an annual car insurance policy to a usage-based policy, realizing they can save a significant amount of money off their standard insurance. LexisNexis conducted a survey of 3,100 UK motor insurance purchasers and learned that the main target group for UBI providers are youthful drivers. The size of this group in the UK is estimated to be one million drivers, 80%–90% of whom have a telematics-enabled policy in place today. According to the survey, an additional 12.8 million drivers are interested in UBI.

Enhanced Claims Processing and Fraud Detection

Streamlining claims processing is another area where big data and machine learning demonstrate their prowess. Insurers employ algorithms to automate claims intake, extract pertinent information from documents, and expedite claims handling. This not only improves efficiency but also enhances customer satisfaction by reducing processing times.

Moreover, big data plays a pivotal role in fraud detection. By analyzing patterns and anomalies in data, insurers can flag potentially fraudulent claims for further investigation. This proactive approach helps prevent financial losses due to fraudulent activities, ensuring the integrity of the insurance ecosystem.

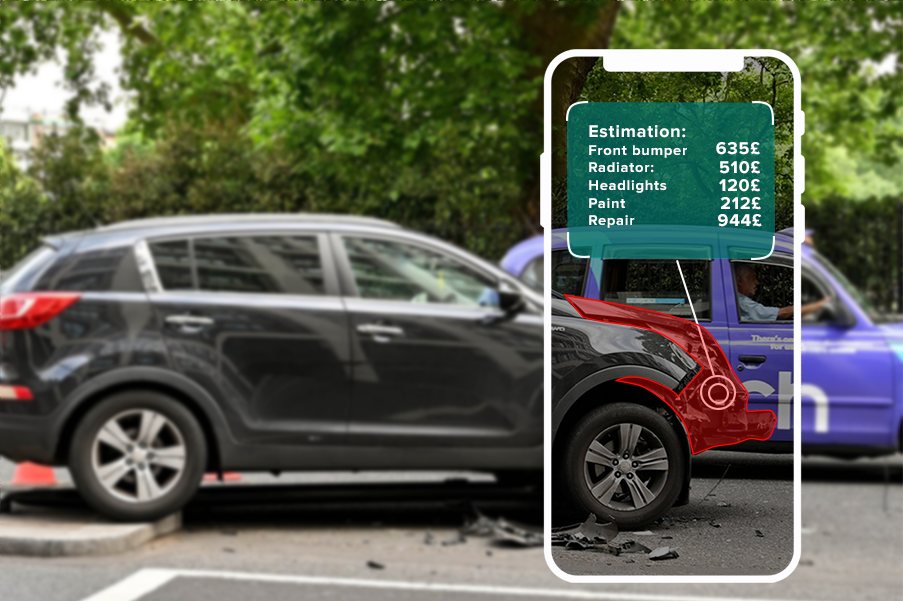

By leveraging big data to assess car damage, claims processing can be expedited, leading to increased customer satisfaction.

By leveraging big data to assess car damage, claims processing can be expedited, leading to increased customer satisfaction.

A great example of using big data and AI to improve claims processing is Tractable. The company uses AI to analyze images of damaged cars and homes to assess the severity of the damage and provide a detailed estimate of the damage cost. Tractable's platform can complete a car damage appraisal in 3 minutes based on FNOL photos. They also claim that thanks to their technology, 70% of claims can be reviewed without human intervention.

Improving Customer Experience

In the digital age, customer experience reigns supreme. Big data facilitates a deeper understanding of customer needs and preferences, enabling insurers to provide personalized services and interactions. Chatbots, AI-powered customer service, and data-driven insights empower insurers to deliver proactive and responsive customer support.

boom by Abacai — Click here to discover the customer story

A great example of using AI to improve customer experience is offered by Abacai's boom. Boom has been designed and built as digital car insurance. The end-to-end customer journey, from providing the client with a quote to processing the claim, is fully digital. To provide policyholders with 24/7 support and great self-service capabilities, the company implemented an AI-powered chatbot available on the mobile app and web portal that can answer questions related to policies and guide the policyholder through the FNOL journey. All of this results in a great customer experience, proved by the 4.8 score Boom app has on the App Store.

Challenges and Ethical Considerations

While the benefits of big data in insurance are substantial, they are not without challenges. Data privacy concerns, ethical use of customer data, and the need for robust cybersecurity measures are critical considerations. Ensuring transparency and obtaining consent for data usage remain imperative to maintain trust and compliance with regulatory frameworks.

The Future Landscape

The role of big data in the insurance industry will continue to evolve. Advancements in technology, including the Internet of Things (IoT) and further sophistication of AI and machine learning, will deepen the industry's reliance on data-driven insights. Additionally, collaborations with tech innovators and the integration of emerging data sources will open new avenues for insurers to innovate their offerings and services. We already see the rise of parametric insurance, with companies like McKenzie Intelligence Services providing insurance companies, brokers, and loss adjusters with insights from their platform analyzing geospatial data to track natural catastrophes.

As we delved into big data, let's not overlook Low-Code as another significant technology. It deserves attention for its ability to build innovative solutions 6 times faster than usual. Interested? Learn more here: Article - The Power of Low-Code in Insurance

In conclusion, big data has transformed the insurance industry from a landscape reliant on historical data to a dynamic field harnessing real-time insights for risk assessment, policy customization, streamlined operations, and enhanced customer experiences. Embracing the potential of big data will be pivotal for insurers to stay competitive and meet the evolving needs of a digitally empowered consumer base.

Looking to discover how your enterprise can apply big data? Check out this page: Solutions for insurance companies or get in touch with our experts!