Share

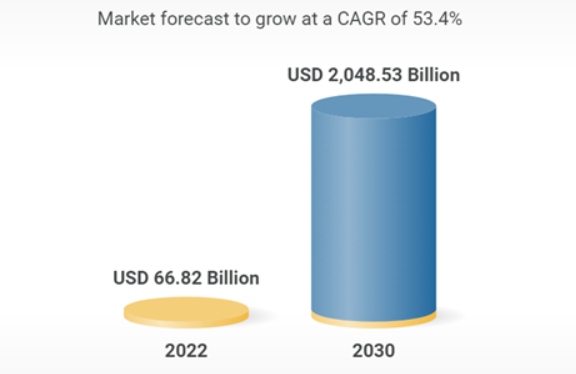

Mobile-first is the new-age mantra for success in the banking industry today. Visiting physical branches seems like ancient history, and even cash transactions may slowly fade into the sunset, thanks to the rise of neo-banking and digital money. Since the coronavirus pandemic hit, the traditionally slow to change banking industry has witnessed massive disruption, owing to the increased dependency on online banking platforms to transfer money and make payments. According to market research store Research and Markets, the global neo-banking market is pegged to touch $2,048.53 billion by 2030, growing at 53.4% (CAGR ) from 2022 to 2030.

The growth of neo-banking is driven by multiple factors, including a more transparent and low-cost structure, faster loan approvals with low-interest rates via banking applications, customized services via mobile apps, increased adoption of advanced tech like artificial intelligence (AI) and IoT, the rising popularity of mobile apps to make international fund transfers, and a conducive regulatory environment. But what really are neo-banks, and how are they different from the friendly neighborhood banks that were the norm? Simply put, neo-banks do not exist in the physical world. Also dubbed internet-only banks, challenger banks, or digital banks, neo-banks operate exclusively online without any traditional physical branch network.

Global Neobanking Market

The Middle East Story: Similar to other regions in the world, the Middle East, too, is witnessing unprecedented disruption with the influx of neo-banking and a new way of dealing with money matters. The growth of the Internet increased smartphone penetration, and a digitally-mature customer base has contributed significantly to this growing trend. It is estimated that about 60% of users in the UAE and Saudi Arabia alone prefer using a banking app for their financial transactions. That said, neo-banking is still in its infancy stage in the Middle East. The potential for neo or digital banking in the region is enormous, as is evident from the expanding investment in the sector. It is expected that in 2022, about 465 fintech firms in the Middle East will raise over $2 billion in venture capital funding, compared to the 30 fintech that managed to raise $80 million in 2017.

State of Banking and FinTech in the Middle East

The banking sector in the Middle East is at an inflection point with the increasing adoption of digital transactions. Estimates suggest that about 50% of the Middle East and North Africa population is still unbanked and financially excluded. This offers a substantial fertile ground for easy-to-use digital apps that provide banking services. Even before the pandemic, digital banking transactions were seeing an uptick in the Middle East. For instance, in the UAE alone, digital payments grew at a rate of over 9% between 2014 and 2019—almost double the 4%-5% growth that Europe saw during the same timeframe. Saudi Arabia's numbers were astounding—the kingdom saw a whopping 70% increase in digital payments from February 2019 to January 2020 alone.

Since the pandemic, these numbers have only grown. According to a McKinsey survey, noncash payments increased by 20% according to 43% of payment practitioners. And the shift to digital is permanent, with 90% of practitioners stating that at least 50% of the new users will continue to use digital payments instead of reverting to cash later. Nations in the region are beginning to comprehend the need to expand their digital banking footprint. Saudi Arabia, for instance, is aiming to become a cashless society and achieve 70% cashless payments by 2030.

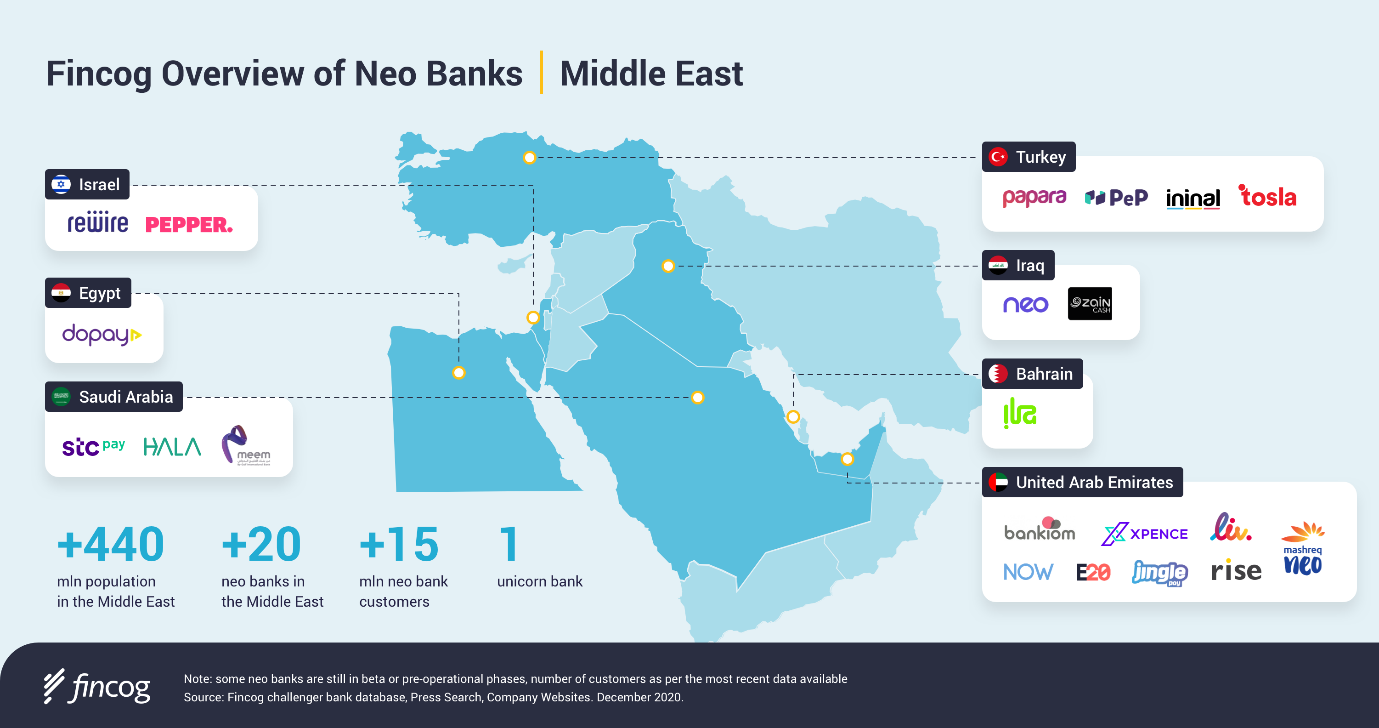

Against this backdrop, the neo-banking sector is slated to see a significant increase in the Middle East, with even established banks beginning to offer digital banking services. Estimates peg the fintech market in the Middle East and Africa to touch $3.45 billion by 2026. In particular, the UAE has seen massive adoption of digital banking owing to the significant ex-pat population (90% of the nation's population). While currently, only a handful of digital banks operate in the region, operating under an established lender's license, such as Emirates NDB's Liv; Mashreq Neo; CBD Now; meem by Gulf International Bank; and Bank ABC, Bahrain's neo-banking, the potential is mammoth.

Industry estimates suggest that UAE leads the pack in the Index of Modern Financial Technologies (FinxAr) by the Arab Monetary Fund, with an average of 75%. The nation is home to 24% of the fintech companies in the region, followed by Morocco and Egypt (12%) and Tunisia (10%).

Opportunities and Challenges to Neobanking in the Region

There are key factors contributing to the exponential increase of challenger banks in the Middle East, the most important of which is a massive unbanked population. According to the World Bank, the Middle East and North Africa region accounts for 1.7 billion people with no access to basic financial services. This, clubbed with the rise of digital payment options, a friendly regulatory environment, and high investment in the fintech sector, is driving the growing neo-banking footprint.

Additionally, the rise of advanced technology, including APIs, artificial intelligence, distributed computing, and blockchain, is reshaping the region's financial sector. And yet, despite the advancements, the fintech and digital banking ecosystem in the Middle East faces major hurdles. While the growth of tech-focused solutions is apparent, the need for additional investment is needed to boost impact. Besides, most of the bank-fintech engagements are exploratory in nature with few strategic partnerships. A Deloitte survey of the relationship between digital leaders and fintech in the Middle East found that only 5% of banks partnered to win while 15% partnered to differentiate.

Designing and developing a challenger bank is not only about taking existing banking processes to the cloud and creating a digital equivalent of the legacy processes. It involves a complete reimagination of banking processes through a digital-only lens across all aspects of the transformation—from customer interactions and employee engagement to risk mitigation and cybersecurity. The impact extends across the entire framework of banking operations, including the front, middle and back offices.

The Road Ahead

As neo-banks bridge the gap between digital and traditional banking, they offer here-and-now services and meet the digitally-savvy customers' expectations. At the same time, they are the easiest and fastest way to enable a digital economy and include large, previously unbanked sections of the population under its ambit. The industry's growth will make it imperative for traditional banks to become increasingly digital banks or lose market share. No surprise then that neo-banking is emerging as a viable alternative to conventional banking and financial services in the Middle East.

By enabling customers to skip the traditional account opening-related paperwork and time-consuming processes, neo-banks help transition to faster, secure, and digital financial services. This at significantly more affordable costs and service fees, higher interest rates, and seamless international payments and money transfers. Besides, neo-banks leverage advanced technology and a conducive regulatory framework to offer wide-ranging financial solutions offering customers a more comprehensive view of their financial health and better control over their finances. Whether it is the Middle East or any other global region, neo-banks are set to usher in the next wave of disruption in the financial industry.